ASEAN Automotive

ASEAN Automotive

As automotive manufacturers around the world continue to grapple with stagnating or declining sales in their traditional markets, a strong strategy for geographic diversification becomes increasingly urgent.

Over the past decade many OEMs had strategies that focused on emerging markets that had obvious growth potential, notably China, India and Brazil. As they review their growth strategies, the case for investment in one of the world's most dynamic automotive clusters – ASEAN – becomes most compelling.

Home to three major automotive hubs and an additional 7 attractive markets, ASEAN is an obvious next step in the growth strategies of automotive manufacturers.

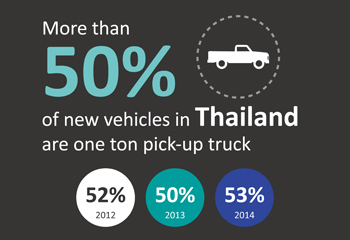

Thailand continues to be the dominant hub within South East Asia, with the best automotive supply and logistics chain as well as impressive production figures for domestic and export markets. Whilst the industry has suffered significantly in recent years, the underlying trend suggests that the industry is close to being back on a growth path. As with other markets, Thailand is moving towards eco cars and SUVs, but the country's industry is still dominated by one ton pick-up trucks.

Thailand continues to be the dominant hub within South East Asia, with the best automotive supply and logistics chain as well as impressive production figures for domestic and export markets. Whilst the industry has suffered significantly in recent years, the underlying trend suggests that the industry is close to being back on a growth path. As with other markets, Thailand is moving towards eco cars and SUVs, but the country's industry is still dominated by one ton pick-up trucks.

Many OEMs and automotive component manufacturers are seeking to develop stronger revenue streams and this is bringing the aftersales market into greater focus. This market offers significant potential to the industry as a strong revenue stream.

Ipsos Automotive Publication – Thailand

Our latest publication on the Thailand Automotive Aftersales market highlights that there will be more than 18 million passenger vehicles in Thailand by 2020, thereby offering an attractive opportunity in the automotive aftermarket arena.

Even though parts quality is the most important criterion for selecting the aftermarket channel, the non-OEM parts has a significant share in the market. Request your copy of the full report here.

With the largest economy in ASEAN, Indonesia expects passenger vehicle growth at a CAGR of 7.4% to 2020. The commercial vehicle sector should also enjoy solid growth.

The Indonesian growth story is not just about Jakarta and Java Island. The 76.2 million motor cycles and 8.3 million passenger vehicles in Indonesia are widely spread across the nation, with the top 4 cities accounting for only 11% of the motorcycle population and 26% of the passenger car population. With this high level of fragmentation, you might want your initial focus to be on Jakarta, due to its higher concentration of vehicles and attractive growth prospects for segments such as MPV as well as "value" vehicles.

While Jakarta is expected to maintain its contribution to national passenger vehicle growth, less developed provinces such as Kalimantan and Sulawesi, have been growing at a faster pace due to demand from first-time owners.

Ipsos Automotive Publication - Indonesia

Our latest paper on the Indonesian Automotive industry presents information that is needed for the development of a Go-to-Market strategy in Indonesia. Request your copy here.